Costco Wholesale Corp. And NVIDIA Corp. A Tale Of Market Schizophrenia

- Paul Robert

- May 31, 2025

- 3 min read

In God (I will praise His word), In God I have put my trust; I will not fear. What can flesh do to me?

Psalm 56:4

As a Christian, I am meant to be bold and courageous and through my humility and discernment, my faith in God should reject fear as both cannot coexist. This is not to be confused with being foolish and reckless. God’s word is truth, and I am able to rest in His truth as I abide in His word. The reality is that my flesh, or emotional state is a constant contradiction to God. Only through a relationship with Jesus Christ as my Lord and Savior can I truly be free from my fleshly desires.

The irony for those who reject having faith in Jesus Christ is that trust and faith are placed into daily activities all the time. Flying on an airplane, driving on a freeway, engaging with people we do not know well, all require degrees of trust. Investing is no different as I must put my trust in people, a company and its partners and customers, the exchange the stock is traded on, and the liquidity of my money based on transactions. Understanding this and recognizing variables of control versus those outside of control and discerning the right strategy and execution are what unlock successful investment performance over time.

Today’s stock market valuation multiples reflect how relevant popularity has become. Inflation has led to high asset prices, and even higher risk asset prices remain extremely overvalued, which is also true for equities where the most popular companies sport some of the highest valuations. As savvy long-term investors already know, this popularity contest won’t last, and many companies will inevitably see their valuation multiples contract.

This is a perfect example of why NVIDIA Corporation (NVDA) and Costco Wholesale Corp. (COST) are trading at near parity despite very different business models and growth rates. Both companies have recently provided quarterly reports and investors have bid COST up to near equal valuation with NVDA based on OCF/Share.

This of course makes no sense and there is no rationale way to justify COST’s valuation level. Even among direct peers COST’s OCF/Share multiple is 76% higher than the next company, Walmart, Inc. (WMT). WMT is the clear number two competitor to Amazon, Inc. (AMZN) based on its omnichannel and e-commerce business services. WMT’s scale is 2.5 times that of COST. Even with AMZN’s AWS and services segments, WMT is trading at a premium to AMZN’s OCF/Share with COST trading double that of AMZN.

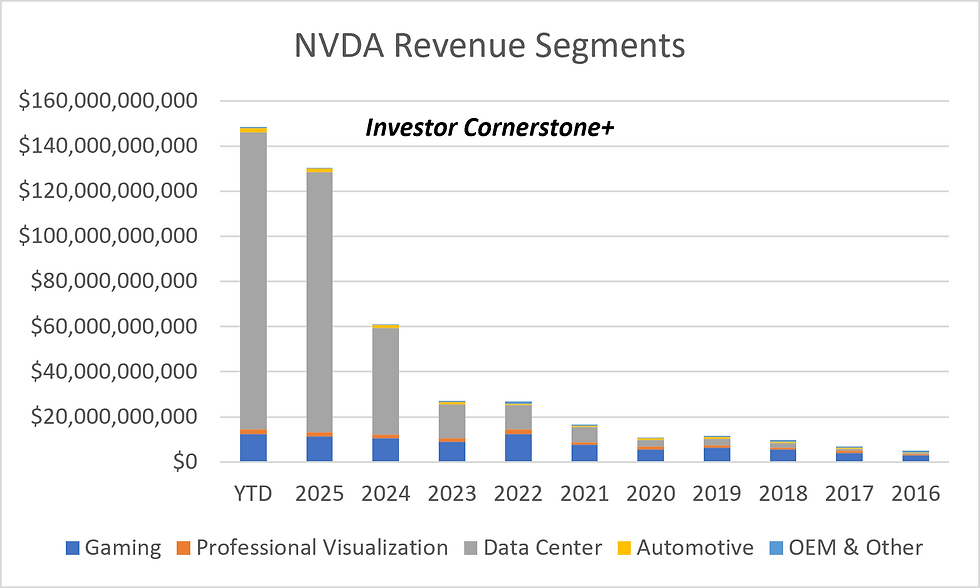

NVDA’s revenue growth continues to impress greatly. NVDA was only generating less than $17 billion in revenue five years ago versus COST’s $163 billion. Over the next three to four years, NVDA will have eclipsed COST’s level generating over $300 billion. With the market’s schizophrenia in mind, what is the rationale as to why COST trade at near-parity with NVDA based on OCF/Share?

Wallstreet has bid up COST as it continues to illustrate robust comparable store growth. Additionally, COST has figured out how to accelerate its e-commerce growth as well. The stock market is placing a higher rate of growth over a longer duration to justify cash flow multiple expansion.

Pre-pandemic, 2016 through 2019, COST’s daily OCF/Share average was 15 times. While valuation multiples can be subjective, COST’s OCF/Share multiple has increased by 150%, which is a fact. Anyone could argue that an average of 15 times cash flow was too low as the company has proven its durability, resiliency, and technological improvability, but the degree of premium has gotten way ahead of these justifiable traits.

COST is a conviction sell at this point. While COST is separating itself within the discount stores category, it does not justify a multiple beyond Big-Tech. Many of COST’s peers trade less than 10 times OCF/Share so double this area already serves as a substantial premium.

NVDA, on the other hand, has been growing into a much more reasonable valuation level with robust revenue growth still anticipated over the mid-term and beyond. The recent pullback to the $100 level was an excellent level for opportunistic investors to initiate or accumulate shares. Even at the current $135 level, NVDA offers solid future upside potential.

Comments