Opendoor & Options

- Paul Robert

- Sep 5, 2025

- 7 min read

For as we have many members in one body, but all the members do not have the same function, so we, being many, are one body in Christ, and individually members of one another.

Romans 12:4-5

The beauty of the Gospel and the church is that there is a collective body of believers that work together and through the Holy Spirit, achieve amazing things. This could be missionaries helping serve impoverished communities in a distant land, or it could be taking the time to help a neighbor’s needs. God has gifted us all with unique abilities and skills and with His guidance the body of Christ is poised to serve.

The landscape has shifted across Wallstreet versus Main Street. Retail investors have become much more segregated as trading has proliferated. In some ways this has given retail investors an ad hoc foothold on influencing stock moves, notably across areas with substantial short interest. In some ways, through this shift, retail investors can relate to being individually members of one another.

Opendoor Technologies, Inc. (OPEN)

OPEN has become a stock of interest as it has achieved ‘Meme’ status. I have covered OPEN since going public and while I recognize that Meme stocks can simply take on momentum that defies logic, OPEN is setting up to be a very dangerous trading option.

Eric Jackson from EMJ Capital is looking to capitalize on OPEN’s volatility, touting the company’s potential to jump towards $100 per share or higher. This is reminiscent of Carvana, Inc.’s (CVNA) meteoric rise from a low below $5 per share at the end of 2022 to today’s current stock price of $370. While CVNA has already generated a massive return, investor sprits are already increasingly envisioning a similar outcome for OPEN.

Mr. Jackson was an early proponent of CVNA and has made it clear that he’s looking for the next big thing ala OPEN. His optimism is sparked by artificial intelligence, or AI capabilities of OPEN’s data (over 200,000 transactions over the company’s history); and transferable or assumable mortgages also being a big opportunity; with the next macro turn for real estate being a catalyst.

Regardless of what investors may be thinking or saying, OPEN’s business fundamentals will need to substantially improve and there are some important questions that deserve to be addressed.

Question 1 – What are OPEN’s Current Fundamentals Telling Us?

The short answer to this is that OPEN’s business model is not innovative enough to substantially penetrate the U.S. existing home sales market. OPEN has struggled greatly to shift much from being a larger home-flipping company. This is clear as OPEN has had to depend on partnerships with companies like Zillow Group, Inc. (ZG) and eXp World Holdings, Inc. (EXPI) to gain access to real estate brokers and agents to incorporate legacy services. OPEN’s marketplace approach has not taken off and the company has deviated from its pure iBuying focus to incorporate offers and agent support from its partnerships.

OPEN’s overall U.S. existing homes sales market penetration has remained flat irrespective of market cycles. The only time OPEN witnessed increasing performance beyond normalcy was during the housing market recession where annualized volumes dropped precipitously during 2022. The peak housing price situation has afforded OPEN increasing revenue, but not enough to improve the company’s fundamentals to any significant degree.

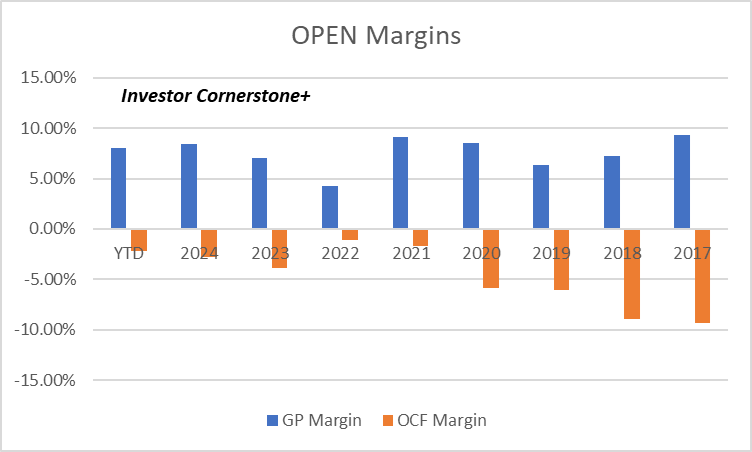

OPEN’s margins have been another area where the company, despite cost-cutting measures, really hasn’t been able to achieve any meaningful success. Gross margin has remained flat and operating cash flow, or OCF margin has continued to be negative by greater than $125 million. OPEN finances its real estate inventory purchases, but the company has recently hit a cash crunch before raising extra funds to delay this risk a little further out.

OPEN fundamentally needs to show that the company has a viable and innovative approach that will lead to market penetration over time. To date, this clearly has not been the case.

Question 2 – How Does OPEN Need To Scale The Business?

OPEN, put simply, needs to purchase and sell more homes. The product does not resonate with most existing home sellers and buyers due to the spreads the company utilizes to hedge risk. This approach failed to offset substantial property write downs during and after the 2022 real estate recession, and management’s most recent response has been to become more conservative with the degrees of spreads based on market seasonality.

Investors need to consider that OPEN is only a niche player within the current 4 million or so annualized homes being sold across the U.S. where special situations for sellers and buyers requiring shorter-term moving timeframes is an area of core focus. This puts further risk on their ability to scale as their addressable market currently for OPEN is substantially below the total.

By contrast, CVNA has been highly successful in growing its volumes after recovering from pandemic effects, while also unlocking cash flow inflection.

While average sales prices for retail and wholesale vehicles have flat-lined of late, CVNA has witnessed robust growth in total vehicle unit sales from the 2023 contraction. This re-acceleration has CVNA back on track for robust growth and contrary to OPEN, CVNA is taking market from legacy peers.

CVNA has witnessed substantially improved gross and OCF margins. While it is debatable as to CVNA being overvalued at today’s stock price, the company has grown significantly into its valuation level providing justification for the 7,300 percent increase over the past few years. If OPEN were to simply jump to $10 per share and continue higher, the disconnect with the company's fundamentals would be an increasingly greater risk to the downside.

If OPEN is to justifiably see a similar stock price increase over the next few years, the company will need to grow its fundamentals substantially higher from the company’s performance over the past eight years. It’s easy to assume that as the real estate market sees a pickup in annualized volume, that OPEN will be able to scale further. But investors should note that this may only get the company back towards 20,000 homes sold or around $7 billion in revenue. Former management guided for $10 billion in revenue to break even on cash flow. For OPEN to become a compelling investment leading to a stock price approaching $50 per share, the company will likely need to be selling closer to 70,000 homes per year.

Question 3 – How Critical Is Management To The Bull Thesis?

Carry Wheeler’s resignation was mixed as those frustrated with OPEN’s performance were looking for a change. However, OPEN has faced concerns since the departure of its founder, as well as with the company’s building of the current executive team. Most, if not all major companies that have innovated based on technology and taken substantial market share within their respective industries have had foundational leadership over a period such as a couple of decades.

For OPEN, the company is completely disconnected from any foundational leadership and those coming in, just as Carry Wheeler did, are not vested and committed deeply to the company’s success. Ms. Wheeler recently sold a large portion of her shares after her exit raking in $35 million because of the Meme phenomenon.

Many new executives that are not wedded to a particular company that come in after-the-fact always seem good on paper. The problem is that most of the time, their tenure is short-lived, and the company is not afforded any significant improvement across business fundamentals.

OPEN is in this exact situation and without any foundational leadership the company is at a high degree of risk of shifting priorities, tweaking of the business model, and reshuffling of team members and initiatives and priorities.

Question 4 – How Can Traders Win With Options?

A primary challenge right now with OPEN is that it isn’t clear as to how traders will win and who will lose. Clearly Mr. Jackson wants to see OPEN go up towards $50 or $100 per share. But this type of price action is highly disconnected from the company’s fundamentals and even near-term expectations.

Clearly based on the chart, OPEN is trying to break out. Breaking out is dependent upon volume and position. If more traders bid up OPEN as those who are short see their positions expire, this leads to the classic ‘short squeeze’. This scenario can last for a while but usually fizzles quickly once markets realize that the company being squeezed is a pretender or the degree of overvaluation becomes too extreme.

A big challenge for traders today is that OPEN’s future moves are highly speculative no matter what way you look at them. Calls, puts, straddles, etc. all are subject to backfire on any given week. This puts most traders at risk of losing money. The broader markets being at all-time peaks do not help either as any event that could trigger a 5-10% correction could serve as an unanticipated headwind.

No matter how you look at it, the real estate market is in a major doldrum. Volumes are low, inventory is high, home prices are still near all-time highs, and mortgage rates remain near 7 percent.

OPEN is extremely speculative and if I were to trade it, I’d wait for the if and when the company would take off to an extreme degree, towards $50 per share. This level would afford a much more solid short position that could consider numerous timing scenarios to mitigate any continued upside extremity. In the $1 to $10 range, OPEN is likely to ebb and flow, which will benefit sophisticated traders, but will probably wipe out a lot of inexperienced investors jumping into this game.

Key takeaways for traders to think about are:

OPEN has not successfully penetrated the U.S. existing home sales market and the company’s fundamentals are weak – OPEN is not close to being a CVNA.

Management is not committed to the business model and there is no foundational leadership.

Short-term speculators are trying to manipulate the stock price to maximize aggressive quick gains – the battle of short/long traders is not clear yet on who will win.

Comments