Conviction Investment Series: Palantir Technologies (June 24, 2025)

- Paul Robert

- Jun 24, 2025

- 4 min read

Updated: Jun 24, 2025

Bearing with one another, and forgiving one another, if anyone has a complaint against another; even as Christ forgave you, so you also must do.

Colossians 3:13

The world can be a difficult place when it comes to relationships. Even the best of relationships can still have moments of disagreement, disfunction, and frustration. But God’s word always rings true, and it is always a reflection of Jesus sacrifice for me. This sacrifice is a constant reminder for how I am meant to conduct myself amid conflict with others, I am meant to forgive. It is easy to make excuses as to why someone may not deserve my forgiveness, but I must always remember that I never deserved Jesus Christ’s sacrifice for me at the cross.

From a social media and investment perspective, forgiveness can be expressed as giving others the benefit of doubt as it isn’t always easy to understand where someone is coming from, or what is driving their investment thesis. Grace can be important to learn as no investment strategy will be perfect with respect to varying management strategies. And having forgiveness can also lead to a stronger sense of humility that can help fight biases against professionals and others on the Internet with differing viewpoints on companies of interest.

I have begun a conviction series on Palantir Technologies, Inc. (PLTR). My conviction is based upon a dichotomy of PLTR’s potential, versus its overvaluation. This series is meant to generate a dialogue regarding how to consider investing in PLTR during its current state of excessive overvaluation. The first blog to this series can be found here. The next part of this series is:

Deconstructing Valuation: Long-Term Versus Momentum

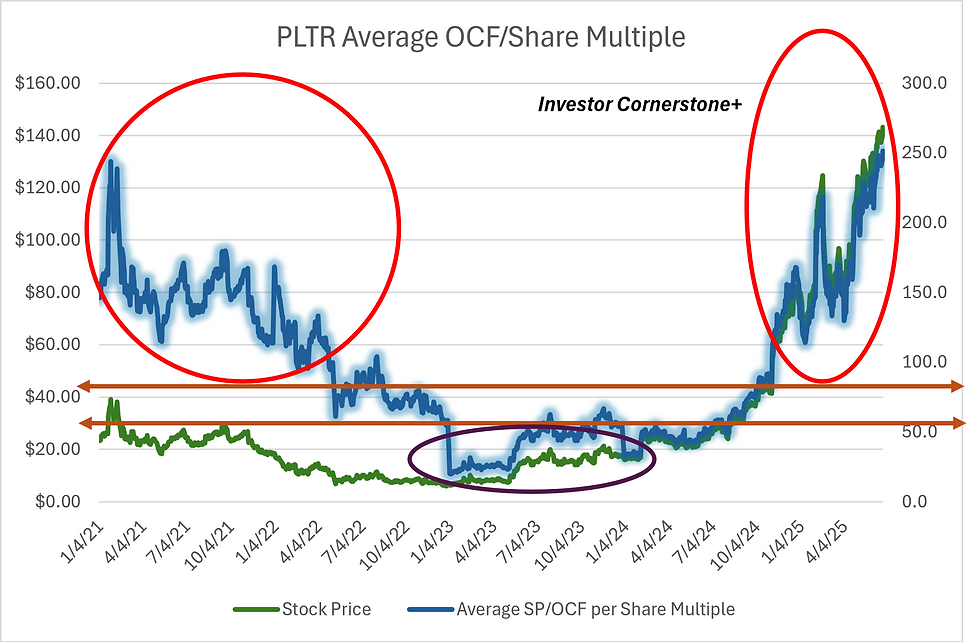

PLTR has been public since 2020 and as a result, has only been an investment option over the last five years. The company has witnessed two short-term periods of momentum investing inflating its valuation. The first time occurred during the pandemic, and the second has been ongoing since 2024. The latter has taken PLTR’s valuation multiples to arguably the most overvalued stock across all U.S. exchanges.

To assess long-term versus momentum implications it is important to recognize just how detached PLTR is from its peer group valuation levels, and equally, how a contracting valuation multiple as time passes by places investors relying on this momentum at risk.

PLTR’s peer group includes a little less than 50 technology software infrastructure and application companies. There are numerous ways to slice and dice valuation comparisons and peer growth expectations. Key indicators include stock price to operating cash flow per share (SP/OCF-Share) and enterprise value to revenue or sales (EV/Sales). Others include operating cash flow margin (OCF Margin), and two-year estimates of previously mentioned indicators.

PLTR’s indicators are as follows:

SP/OCF-Share: 243 times

EV/Sales: 103 times

OCF Margin: 43%

Two-Year SP/OCF-Share: 142 times

Two-Year EV/Sales: 58 times

Five-Year Average Sales Growth Est.: 35%

Five-Year Average OCF-Share Growth Est.: 37%

OCF/Share Average Price Target Growth: 0.6%

Of this peer group, only one company trades with a higher current SP/OCF-Share multiple, PLTR trades nearly 3 times higher on current EV/Sales to the next closest peer, for two-year estimates, PLTR trades higher than any other peer for SP/OCF-Share and over two times higher for EV/Sales, PLTR ranks fourth out of this group based on OCF Margin, second on the five-year Average Sales Growth Est., and third on the five-year Average OCF-Share Growth Est. Aside from Microsoft Corporation’s (MSFT) $3.5 trillion enterprise value, PLTR is second to none on this list at $333 billion.

To the latter points of revenue and OCF-Share growth, bullish investors claim that the stock price is justified. The belief is that the fastest growing companies deserve the highest premiums and will grow into their lofty valuations over time. Many investors believe that PLTR will become a trillion-dollar company as the company is already a third of the way there.

The problem is that most of the trillion-dollar Big-Tech companies today are doing tens of billions in cash flow generation, which in most cases will remain greater and even exponentially greater than PLTR’s estimated 2029 revenue. A primary difference with long-term aggressive growth investing and momentum is the former focuses on building reasonable positions in companies with strong upside potential. The latter tends to succumb to emotionally driven actions based on speculation and hype. During the ‘good times’ it is easy to defend momentum, but when the tables turn, many investors get burned.

A big risk for investors today is looking at companies like Cloudflare, Inc. (NET), CrowdStrike Holdings, Inc. (CRWD), Snowflake, Inc. (SNOW), and Zscaler, Inc. (ZS) among others as while they have substantially lower valuation multiples than PLTR, they remain highly overvalued despite slower growth expectations. Investors who may think that PLTR’s slowing growth should still equate towards 100 times OCF-Share because some of these peers are trading near or higher than that level, may be in for an uncomfortable surprise.

The key to long-term investment success for aggressive growth opportunities is to identify potential winners early. Momentum, whether more broadly across markets or isolated to a specific company will always end up making a one-eighty-degree turn. This is especially true for markets and/or companies that are excessively overvalued.

PLTR is trading on nothing but exuberance at this point. It does not matter what the valuation is, nor does it matter what the company announces. There is no piece of information or analysis that can influence the market to sell the stock lower as greed to maximize short-term gains before the tables turn remains the focus. PLTR will drop at some point and offer long-term investors that remain patient, a much better entry point.

Comments