Can Mercadolibre Become Latin America’s First Trillion Dollar Company?

- Paul Robert

- May 29, 2025

- 3 min read

But the mercy of the Lord is from everlasting to everlasting

On those who fear Him,

And His righteousness to children’s children,

To such as keep His covenant,

And to those who remember His commandments to do them.

Psalm 103:17-18

What does it mean to fear the Lord and how am I to keep His covenant. God’s mercy is the key. God extended His mercy by His covenant to the people of Israel to give them a hope and future with Him. He created a new covenant extending mercy through the death and resurrection of Jesus Christ for all who put their faith in Him. This mercy is from everlasting to everlasting and covers my inability to perfectly uphold God’s laws and commandments.

Investing similarly follows a traditional pattern with rules and standards that are meant to be followed. Wallstreet is the orchestrator of these rules as investors are pressured to accept P/E ratios, stock buybacks and business deals as standards and norms. Unlike God’s covenant and the Gospel of Jesus Christ which is based on perfect laws and God’s holiness and righteousness, Wallstreet’s structures are imperfect and misguided towards greed and self-interests. While God’s mercy is the key to meeting His standards, Wallstreet’s standards are not meant to be followed as they are flawed to begin with.

Mercadolibre, Inc. (MELI) is an amazing success story. Since 2008 (a 17-year period), MELI’s revenue has grown by 16,235% or an annualized 35%. OCF/Share has grown an astounding 47,220% or an annualized 44%. The stock price has increased by 15,900% or an annualized 35% consistent with revenue performance. This suggests undervaluation as OCF/Share performance is typically more strongly correlated with stock price performance.

Ironically, this undervaluation is pertinent to the topic of can MELI become Latin America’s first trillion-dollar company; based on today’s valuation, the company already trades at a valuation level consistent with Big-Tech.

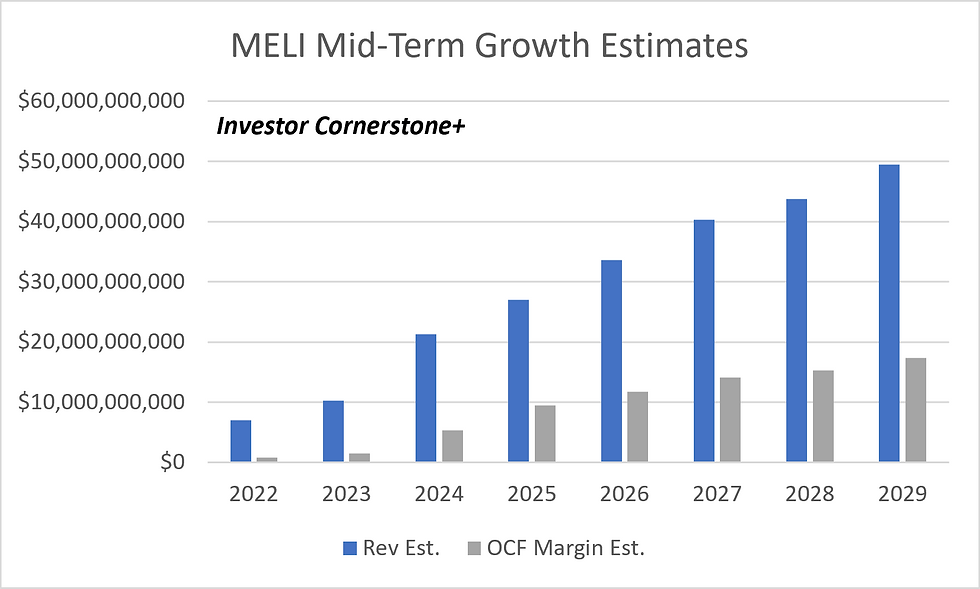

A key trait and characteristic of all Big-Tech peers is their ability to continue to grow revenues robustly even as they scale. MELI is quickly becoming a much larger entity within Latin America, and this sets the company up for the potential for sustained revenue growth towards the $50 billion level over the mid-term. If indeed MELI reaches this level, the stages are set for the company to track higher towards the $100 billion level.

At MELI’s current multiple valuation the company could be headed towards a $350 billion EV at $50 billion in revenue. Longer-term, it is possible that MELI could continue to grow towards the $150 billion revenue level that would potentially afford a $1 trillion EV.

Amazon, Inc. (AMZN) and eBay, Inc. (EBAY) were completely unsuccessful in penetrating the Latin America market. Sea Ltd., (SE) has faced equal issues in attempting to make inroads. MELI continues to illustrate just how difficult it is for foreign companies to establish a brand and take market. At the same time, MELI continues to diversify its products and services, and the virtuous cycle of their scale is compounding.

Near all-time stock price highs, investors should exercise some caution. MELI has a history of outperforming and achieving results beyond Wallstreet’s expectations, and as new stock price highs are achieved, and irrespective of valuation discounts, the market has tended to second-guess the company’s future potential. Additionally, Latin America is prone to currency devaluation, higher inflation and labor unrest, and other regulatory and legal aspects that can add to short-term pressures on MELI.

With these risks in mind, and the current broader stock market levels, investors may want to wait for a pullback.

Comments