Alphabet - It's A Numbers Game

- Paul Robert

- May 18, 2025

- 2 min read

But the wisdom that is from above is first pure, then peaceable, gentle, willing to yield, full of mercy and good fruits, without partiality and without hypocrisy. Now the fruit of righteousness is sown in peace by those who make peace.

James 3:17-18

It is reassuring how God begins a thought about me. It doesn’t start with what I’ve done wrong, and it isn’t based on my imperfections. Instead, God as my creator, shows His kindness towards me first through His truth, and then through His desire for a relationship with me. God’s love is evidenced through His peace and love, fully exercised by the cross at which Jesus Christ paid for the sins of death – our Father in heaven is the true peacemaker.

Peace is seemingly an oxymoron when it comes to investing. Chaos is a term that resonates more closely with investing and the stock market. But chaos tends to be a form of human-derived variables that are inconsistent and/or at odds with one another. This is nothing new and, in many ways, quite common across human interaction and engagement. Thus, peace amidst the chaos can be achieved, and like the qualities of Christ, necessitate that of a peacemaker.

Alphabet, Inc. (GOOG) is the world’s single largest digital advertising company. The growth of this engine of GOOG’s business has been a core driver ever since the IPO more than twenty years ago and still to this day. With the promises and tunnel vision focus being pushed by Wallstreet with artificial intelligence, or AI, GOOG has found itself on the more critical side with questions about the company’s foray into this area. But there are other areas of concern as well, notably, anti-competition concerns and slowing advertising growth.

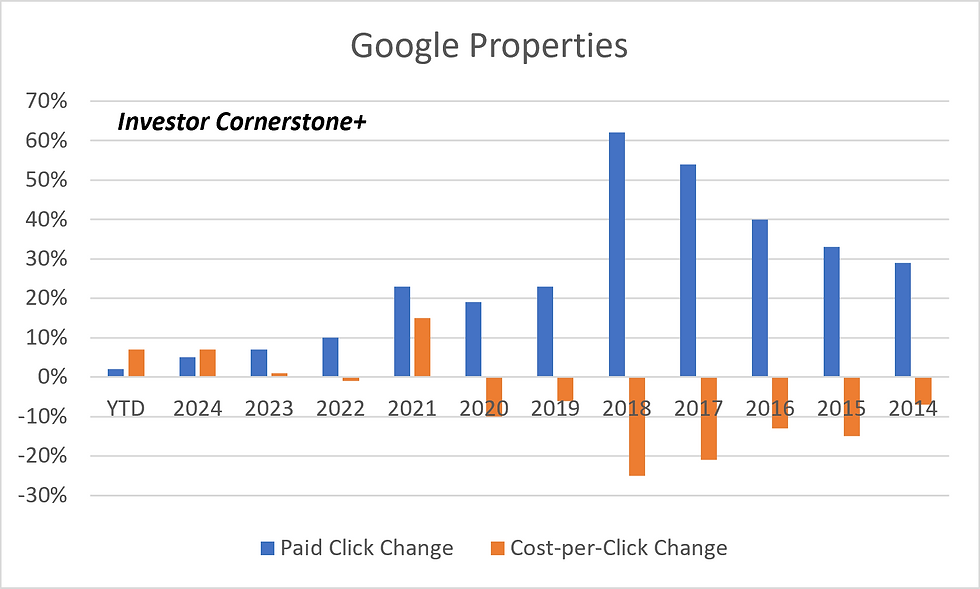

As mentioned, 75 percent of GOOG’s revenue is from advertising revenues. This proportion continues to decline, but the pace of decline also continues to slow. Most of these revenues come from Google Properties like Search and YouTube. And as can be seen above, during the Pandemic a major shift occurred where pack click changes have succumbed to cost increases emerging as the core driver.

This is not a major cause for concern as GOOG will likely still grow through varying degrees of paid clicks and cost increases with the expectation of an overall slower growth cadence. But with concerns over the company being broken up and faster growing segments losing capital investment from the primary cash cow; and less of a revenue bump with AI; Wallstreet has become more bearish in the short-term.

This equates to a numbers game where Wallstreet is looking for the right amount of performance across each of GOOG’s core revenue segments. Valuation multiples tend to be subjective, but since 2017 (the past 2,100 days), GOOG’s OCF/share multiple daily average has been at 16 times. The days of GOOG trading 20-30 times cash flow are likely behind us and investors need to temper investment returns accordingly. The good news for investors is that the stock market has pushed GOOG to a level that still offers solid risk-reward upside potential, even when factoring for these areas of scrutiny.

Comments