MP Materials – Apple Deal Adds Fuel To The Fire

- Paul Robert

- Jul 15, 2025

- 4 min read

But He answered and said, “It is written, ‘Man shall not live by bread alone, but by every word that proceeds from the mouth of God.’ ”

Matthew 4:4

The Bible is truth evidenced both by its proven history and its prophetic accuracy. The divine aspect of the words of the Bible are synonymous with ‘the mouth of God’. As a believer of the Bible, Jesus Christ is the connection between the history and prophecies of the Old Testament to the history of the New Testament. God is the creator of all and as such, His words are just as powerful and essential with respect to all aspects of life.

This verse is directly applicable to investing in that God has a lot to say on the subject of money. A statement that often is misquoted and associated with the Bible is that ‘money is the root of all evil’, when the Bible states that ‘the love of money is the root of all evil’. The Bible has a substantial number of verses focused on money and as God is the provider of everything, being a steward of the financial resources bestowed upon me is a large part of my responsibility.

MP Materials

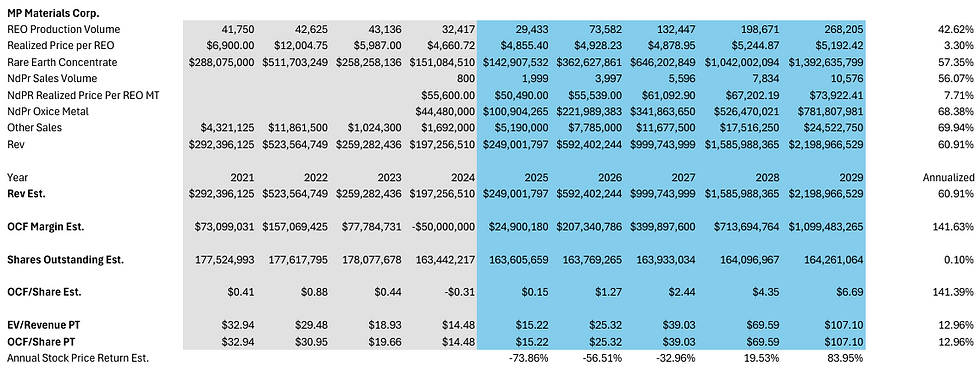

MP Materials Corp. (MP) has been on a wild ride ever since going public through a reverse stock merger, also known as a Special Purpose Acquisition Company, or SPAC. The Average OCF/Share Multiple is a great tool for both long- and short-term investors as it provides a valuation gauge that serves as a means of clarity in an ever-increasing volatile and disconnected stock market. As valuation levels over time become clearer, this tool helps investors recognize buying and selling opportunities.

The problem with a mining company like MP is that at lower scale, the company’s cash flow can fluctuate substantially and with MP’s short-term gyrations in production and sales volumes and realized pricing, the associated cash flow multiple has been less clear to allow investors the timeliest information in relation to MP’s stock price fluctuations.

Sell signals are displayed in red and it can clearly be seen that MP has illustrated both high and low stock price trends with both periods seemingly illustrating overvaluation. The latter has been driven by a substantial decline in gross and cash flow margins combined with sharply declining revenue since the 2022 peak.

Despite the current challenges, MP’s stock price has doubled over the past month to just over $58 per share, equating the company’s previous all-time stock price high. This surge has been driven largely by U.S. Dept. of Defense agreement announcement solidifying the company’s continued expansion of production across the U.S., and most recently, the announcement of Apple Inc. (AAPL) $500 million deal to buy rare earth magnets from MP. Additionally, with the current Administration’s stance against China, MP is getting an added expectation of importance, that likely can be carried forward regardless of Administration change.

While all this news is being used to skyrocket the stock price, savvy investors need to think about the company’s future and how far it may be getting ahead of itself. The simple fact remains that MP is still a mining company, and the commoditized nature of any mining company has its valuation levels that will come into play. As an example, Southern Copper Corporation (SCCO) trades 6.5 times EV/Sales and 17 times OCF/Share. Investors will be hard-pressed to expect MP to trade at a premium as the company scales. SCCO generates $12 billion in annual revenue and $4.5 billion in OCF as a frame of reference.

When considering a highly optimistic scenario where MP grows revenue from the $200 million level to a greater than $2 billion level over the mid-term, investors should be cautious as the market’s doubling of the stock price has eroded a lot of investment returns at near $60 per share, placing greater risk on execution over time.

Like SCCO, MP’s OCF/Share multiple likely will settle in the 15-20 range, and as the company scales over the long-term, the OCF margin will ebb and flow based on factors impacting margins. Additionally, the company’s global market penetration will remain as a minority even with the increasing investment by the U.S. Dept. of Defense and realized pricing will remain a less clear variable as part of the company’s production and sales volume growth.

The run-up is too fast and quick in my opinion; although in a bull market, the run-up could continue further as Palantir Technologies, Inc. (PLTR) has shown. Investors need to be highly cautious currently as Wallstreet looks to push the perceived next big opportunity to levels beyond reason for two reasons. First, they can maximize short-term gains to the extreme, and second, when the bottom falls out, they can conversely benefit from shorting these companies by cutting their stock prices in half or greater.

The trading patterns of the stock market are shifting as influences of artificial intelligence, or AI, social media, and nefarious tactics of disinformation combined with increasing uncertainties such as tariff policies, geopolitical events, wars, etc., are impacting both Wallstreet and Mainstreet.

Pre-pandemic stock market fluctuations, post-Great Recession imbued more cyclical, bull/bear market patterns with less volatility, whereas the past five years have displayed increasingly more volatile and extreme trading patterns over a much shorter period, notably through excessive valuation multiples. This new trend should have investors on guard with the need to consider timing and execution strategies more meticulously. Depending on the pace of scaled production and execution for MP, in a less optimistic scenario, today's stock price could end up generating a 'dead money' outcome.

Comments