FedEx Corporation – Dead Money Since 2017

- Paul Robert

- Jul 5, 2025

- 4 min read

You shall not take vengeance, nor bear any grudge against the children of your people, but you shall love your neighbor as yourself: I am the Lord.

Leviticus 18:19

This is a great Bible verse as it clearly illustrates the consistency of the Old and New Testament. The statement to love my neighbor as myself is consistent with Jesus Christ’s teachings, being one of the most important ways to summarize the Ten Commandments of the Bible. Who is my neighbor? It is anyone who is in need that I know or am aware of.

For investing there are a couple of ways to consider this verse’s applicability. First, it is always important not to develop a bias against professional or peer investors that may misinterpret the potential of a company as time passes by. Second, it is equally important not to become too fixated on the possibilities of a company where there may be controversy. When I’m patient and recognizing where investors with different opinions are coming from and scrutinizing companies with red flags, I tend to make much better decisions.

FedEx Corporation (FDX)

FDX has gone through numerous big moments in the past decade including the acquisition of TNT Express in Europe, to the more recent restructuring of the FedEx Express and Ground operating segments. For investors purchasing FDX 8 years ago, they essentially would have witnessed a ‘dead money’ scenario.

While traders may not be as concerned with mid- and long-term stock performance, longer-term investors would prefer to avoid companies illustrating results like FDX. The challenge is that FDX is a major freight integrator and like the United Parcel Service (UPS), many investors are easily tempted to take a position whether based upon promised margin improvement from management, or simply as a reactive refuting of those with less positive expectations for these major players.

The past decade provides investors with clear problematic areas for the company, including a few areas that investors should have been paying attention to. For those who think that FDX’s weaker performance may offer future potential over the next 5-10 years, focusing on these same indicators will be key.

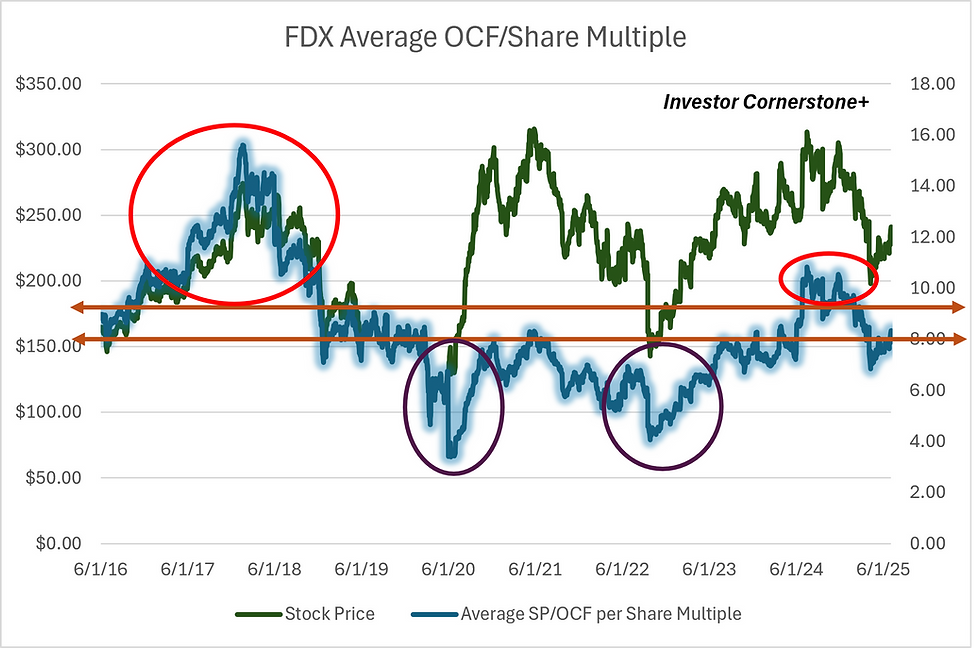

There have been two periods that caught investors off guard. First, after the TNT Express deal, FDX was ascribed a higher valuation multiple due to the anticipated synergies and greater market penetration. This was also combined with FDX pushing for improved margins through the FDX Express segment. But just before the pandemic, questions were already arising and FDX was illustrating some cracks post-deal during the 2019 freight recession.

Second, the pandemic had the opposite effect as FDX like many freight companies benefitted greatly from increased freight rates stemming from supply chain instability. This led to an inverse relationship with valuation multiples dropping, while the stock price increased due to inflationary effects that were not sustainable. Once this realization was clearer, FDX’s stock price dropped again.

The good news is that FDX’s valuation level and stock trading pattern since 2023 have normalized as the market most recently has illustrated a more conventional trend across overvaluation and retrenchment.

While tariff issues have become increasingly problematic during 2025, FDX’s issues have been ongoing since the TNT Express deal. This has made it difficult for investors buying shares over the mid- and long-term as FDX's valuation has been inflated much of the time, leaving investors with narrower windows of opportunity to purchase shares at a reasonable price.

The core culprit for FDX's woes has resulted from declining market share and contracting FDX Express margins. FDX initially attempted to masque this with the TNT Express deal, the pandemic also provided an extended period of masking these issues, and FDX has once again attempted to muddy the waters with the merging of its Express and Ground operations.

Based on FDX’s newly combined Express segment, the trend of average daily volume, or ADV, illustrates a more economically driven pattern of growth. But when we deconstruct the operating segments and their ADV excluding the Ground segment, most have declined since 2017 including U.S. Priority and Deferred, and most notably, International Domestic which resulted from TNT Express deal.

This is a testament to the market’s earlier skepticism of the TNT Express acquisition during 2019, but conversely, FDX's stock price has had moments of extreme inflation due to the market’s continued desire to see FDX succeed from its scale and publicly perceived reputability. The short-term trading strategies of the market are akin to the Wall Street game and investors always need to be on the lookout for companies, especially legacy businesses, that can very easily be manipulated.

On FDX’s freight side, the same trends can be seen aside from the Ground business. There is a combination of many competitive variables, whether from less-than-truckload players like Old Dominion Freight Lines (ODFL) or broader logistics peers like Amazon, Inc. (AMZN), or even the more recent UPS win against FDX for the United States Postal Service contract.

Competitors have taken market share from FDX and UPS for that matter, which has led to a higher focus for FDX on primary trade lanes and commodity mixes. This has been a major deadweight on FDX’s operating margins, most notably for the FDX Express segment leading management to restructure the business and to shift investor focus.

Even at the shipment level, FDX has continued to see significant freight weakness over the past 8 years. By incorporating the Ground segment into the FDX Express segment, the company now can paint a more positive picture and establish a more upbeat narrative for the company’s prospects. This pattern of clear underperformance from important revenue drivers like shipments and tonnage, and management’s decisions to make major acquisitions and restructure are red flags that all investors should be paying attention to.

Over the past near-decade, for mid- and long-term investors, FDX has not been an ideal investment to simply buy and hold. For traders, it has been a perfect company to exploit because the management team has struggled to improve the company’s core metrics.

Depending on investor objectives, there are numerous transportation companies with exposure to freight industries that may offer better risk/reward profiles and investment returns. For those long or short wanting to keep FDX as a consideration, investors should continue to stay laser-focused on FDX’s cash flow multiples to monitor any deviation from trends of normalcy towards over- or under-valuation and take actions accordingly.

Comments